新用戶掃碼下載

新用戶掃碼下載

掃碼下載APP

及時接收考試資訊及

備考信息

轉(zhuǎn)移定價(transfer price)知識點在ACCA歷年考試中頻率很高。一般來說,簡單的考核方式會給出一些條件讓考生判斷產(chǎn)品的外部需求是否已經(jīng)滿足,工廠是否已經(jīng)滿負(fù)荷運(yùn)轉(zhuǎn),這些情況下應(yīng)該選用可變成本還是市場價格來定價。做這類題目的時候需要從集團(tuán)利益的角度的出發(fā),考慮部門之間應(yīng)該采取內(nèi)部購銷還是各自從外部購入或?qū)ν怃N售。總之,做出的決策和制定的價格既要滿足集團(tuán)的利益又不能影響各部門的績效考評。下面我們來看一下2011年12月Q2這道例題,雖然年份比較久遠(yuǎn),但是非常經(jīng)典,難度也比較大,可以說考出了F5績效管理的精髓。

Bath Co is a company specialising in the manufacture and sale of baths. Each bath consists of a main unit plus a set of bath fittings. The company is split into two divisions, A and B. Division A manufactures the bath and Division B manufactures sets of bath fittings. Currently, all of Division A’s sales are made externally. Division B, however, sells to Division A as well as to external customers. Both of the divisions are profit centres.

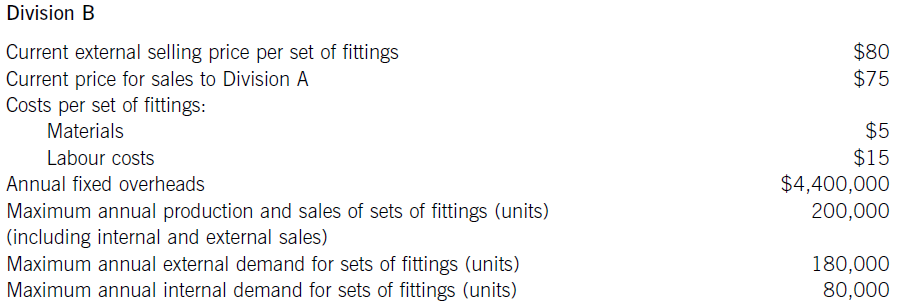

The following data is available for both divisions:

The transfer price charged by Division B to Division A was negotiated some years ago between the previous divisional managers, who have now both been replaced by new managers. Head Office only allows Division A to purchase its fittings from Division B, although the new manager of Division A believes that he could obtain fittings of the same quality and appearance for $65 per set, if he was given the autonomy to purchase from outside the company. Division B makes no cost savings from supplying internally to Division A rather than selling externally.

Required:

(a) Under the current transfer pricing system, prepare a profit statement showing the profit for each of the divisions and for Bath Co as a whole. Your sales and costs figures should be split into external sales and inter-divisional transfers, where appropriate. (6 marks)

(b) Head Office is considering changing the transfer pricing policy to ensure maximisation of company profits without demotivating either of the divisional managers. Division A will be given autonomy to buy from external suppliers and Division B to supply external customers in priority to supplying to Division A.

Calculate the maximum profit that could be earned by Bath Co if transfer pricing is optimised. (8 marks)

(c) Discuss the issues of encouraging divisional managers to take decisions in the interests of the company as a whole, where transfer pricing is used. Provide a reasoned recommendation of a policy Bath Co should adopt.

答案解析

首先,我們要明確題目中部門A和B分別代表什么角色。B是生產(chǎn)產(chǎn)品所用輔料的一方,A需要采購輔料來生產(chǎn)主要產(chǎn)品然后對外銷售。B部門既銷售給A又對外部銷售。瀏覽題干是,我們需要注意Division A 數(shù)據(jù)中的Fitting from Division B 75美元這個金額,它對B來說是銷售收入,而對A是采購成本。Division B 的對外銷售金額80。另一個重要信息點是Maximum annual production and sales of sets of fittings (units) 200,000,Maximum annual external demand for sets of fittings (units) 180,000,Maximum annual internal demand for sets of fittings (units) 80,000。這句話的意思是滿足內(nèi)外部總需求的產(chǎn)能是200,000個單位。A部門需求80,000,而外部需求是180,000,我們需要考慮先對外銷售還是內(nèi)部轉(zhuǎn)移。如果優(yōu)先滿足內(nèi)部需求80,000,那么只能對外銷售120,000;如果先滿足外部需求180,000,那么內(nèi)部只能供應(yīng)20,000。

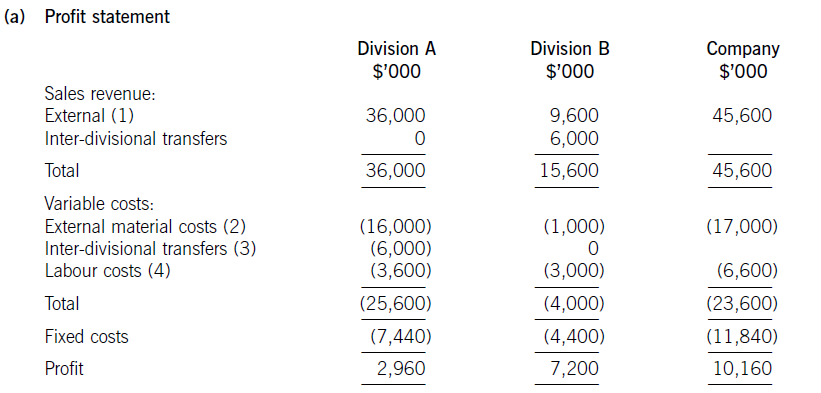

接下來我們先看一下官方給出的答案:

Workings ($’000)

(1) External sales

Div A: 80,000 x $450 = $36,000

Div B: 120,000 x $80 = $9,600

Div B: 80,000 x $75 = $6,000

題目中給出的信息是優(yōu)先滿足內(nèi)部需求,所以先銷售80,000給A部門,收入是80,000 x $75 = $6,000。剩下的產(chǎn)能(200,000-80,000=120,000)分配給外部市場,賺取的收入為120,000 x $80 = $9,600

(2) External material costs

Div A: 80,000 x $200 = $16,000

Div B: 200,000 x $5 = $1,000

(3) Inter-divisional transfers

Div A: 80,000 x $75 = $6,000

(4) Labour costs

Div A: 80,000 x $45 = $3,600

Div B: 200,000 x $15 = $3,000

網(wǎng)校為廣大學(xué)生提供免考科目預(yù)評估服務(wù),您可以點擊![]() 進(jìn)行評估申請。

進(jìn)行評估申請。

關(guān)注“ACCA考試輔導(dǎo)”微信公眾號,獲取更多訊息

歷年樣卷

考試大綱

詞匯表

報考指南

考官文章

思維導(dǎo)圖

新用戶掃碼下載

新用戶掃碼下載安卓版本:8.8.30 蘋果版本:8.8.30

開發(fā)者:北京正保會計科技有限公司

應(yīng)用涉及權(quán)限:查看權(quán)限>

APP隱私政策:查看政策>

HD版本上線:點擊下載>

官方公眾號

微信掃一掃

官方視頻號

微信掃一掃

官方抖音號

抖音掃一掃

Copyright © 2000 - www.sgjweuf.cn All Rights Reserved. 北京正保會計科技有限公司 版權(quán)所有

京B2-20200959 京ICP備20012371號-7 出版物經(jīng)營許可證 ![]() 京公網(wǎng)安備 11010802044457號

京公網(wǎng)安備 11010802044457號

套餐D大額券

¥

去使用 主站蜘蛛池模板: 欧美牲交a欧美牲交aⅴ一 | 亚洲综合伊人五月天中文| 人妻精品动漫h无码| 久久夜色精品国产亚洲av| 国产精品国产三级国快看| 国产亚洲精品一区二区不卡| 国产精品成人中文字幕 | 亚洲免费视频一区二区三区| 国内不卡一区二区三区| 亚洲人成网站免费播放| 日韩中文字幕v亚洲中文字幕| 人妻少妇精品视频专区| 97一区二区国产好的精华液| 91老熟女老女人国产老| 久久99国产精品久久99小说| 久热中文字幕在线精品观| 久久精品人人槡人妻人人玩av| 手机看片福利一区二区三区| 成人精品日韩专区在线观看| 免费无码观看的AV在线播放| 国产免费无遮挡吃奶视频| 精品一区二区中文字幕| free性开放小少妇| 无套内谢少妇一二三四| 国产第一页屁屁影院| 宁强县| 91老熟女老人国产老太| 无码激情亚洲一区| 久久精品国产色蜜蜜麻豆| 激情动态图亚洲区域激情| 亚洲成人av综合一区| 国产精品亚洲综合色区丝瓜| 国产在线精品欧美日韩电影| 国产综合一区二区三区麻豆| 亚洲综合国产精品第一页| 欧美成人VA免费大片视频| 国产网红女主播精品视频| 一区二区三区国产偷拍| 亚洲人成人网站色www| 偷拍专区一区二区三区| 国产成人无码一区二区三区在线|